Twin Cities Habitat for Humanity

Twin Cities Habitat for Humanity

What Does COVID-19 Mean for Your Credit Score?

Credit is one of the most important elements of your financial well-being. It can make all the difference for your life goals, like getting a new...

Understanding key financial terms is essential for first-time homebuyers (and anyone else getting ready to borrow money from a lender). Knowing what these terms mean and what a lender may be looking for can help you in all aspects of your financial life, whether you’re buying a house, buying a car, consolidating debt, or just trying to learn more about your financial well-being.

When you express interest in Twin Cities Habitat’s homeownership program, you will be asked about your income, debt, credit score, and debt-to-income ratio. Below we'll define these terms and share resources and examples to help you find, identify, calculate, and understand these important figures.

Remember, this information pertains to the Twin Cities Habitat for Humanity Homeownership Program. The information in this article may vary slightly from how other associations, lenders, and programs define, calculate, or use these numbers.

Income is defined as "money received, especially on a regular basis, for work or through investments or assistance." There are two basic types of income: Gross income and net income.

If you are employed by a business, company, or institution, to qualify for Twin Cities Habitat's Homeownership program, we ask you about the gross income for your household. If you are self-employed, we must consider your net income.

The income you report on the eligibility form (and later on your application) should include the income of any adults that will be living in the home with you (that's anyone 18 years old or older). You should report income from full- and part-time jobs, self-employment, and seasonal or contract work.

Any financial assistance received by a member of your household should also be included in your total income. This includes things like Supplemental Security Income (SSI), Social Security Disability Insurance (SSDI), Social Security payments, and County Assistance.

Do not count money received for food stamps or employment income from children under the age of 18. Payments received for care of foster children and adoption assistance are also excluded from your income calculation.

Have other sources of income and wondering about how it might affect your income eligibility? Call our Programs Information Center at 612-504-5660.

You can find your gross income on pay stubs from your employer. If you're self-employed or work on a contract basis, your income will be reported on a Schedule C as part of your taxes.

For salaried positions, you can simply use your annual salary number.

(ex: $32,000/year)

For hourly employees: Hourly rate x hours per week x 52 weeks per year = Gross annual income

(ex: $15.00 x 35 hours per week x 52 weeks per year = $27,300 gross annual income)

Tip: Once you have calculated your gross annual income, take that number and divide it by 12. This number is your monthly gross income. (ex: $27,300/12 months = $2,275 gross income/month) This number will come in handy in calculating your debt-to-income ratio later.

Debt is defined as money owed by one party (the borrower or "debtor"), to a second party (the lender or "creditor").

You may already know what monthly loan payments you are making. If you are not sure what loans you have, you can request a credit report to view current loan information and see your credit history.

You can request a copy of your credit report by visiting annualcreditreport.com. (Keep in mind that your credit report is not the same as your credit score, which we've explained in a section below.) This is a free service and a trustworthy place to get your credit report. Here, you can request a copy of your credit report from each of the three credit bureaus. Each person may request one free report (per 12-month period) from each bureau.

You can request a copy of your credit report by visiting annualcreditreport.com. (Keep in mind that your credit report is not the same as your credit score, which we've explained in a section below.) This is a free service and a trustworthy place to get your credit report. Here, you can request a copy of your credit report from each of the three credit bureaus. Each person may request one free report (per 12-month period) from each bureau.

Note: During the COVID-19 pandemic, Equifax, Experian, and TransUnion are offering free weekly credit report checks through April 2021. Visit annualcreditreport.com to access yours.

WATCH: Understanding Credit and Your Credit Report [VIDEO]

These reports will list what money you have borrowed, where you borrowed from, and what you currently owe. Items like your credit cards, student loans, car loans, etc. will be accounted for in this report. Sometimes the information on your credit report is not correct, so check carefully to make sure there are no mistakes. If there are mistakes, you can dispute them. Learn how on the Federal Trade Commission’s website.

You can use this information to calculate your total debt by adding up all outstanding debts.

(ex: Car Loan: $10,500 + Credit Card: $400 + Furniture Loan: $2,000 = $12,900 total debt)

Tip: Add up your monthly payments for each loan or account to get your total monthly debt. This number will be used in the debt-to-income section.

(ex: Car Loan: $200 + Credit Card: $25 + Furniture Loan: $105 = $330)

There are some local organizations that can assist you with pulling, reading, and understanding what your credit report says. During the tax season, if you qualify for their services, you may be able to access the Financial Services offered at Prepare + Prosper tax clinics.

Remember when we recommended that you calculate your monthly debt totals earlier? This is where it pays off! Your debt-to-income ratio (DTI) tells lenders how reliably you pay off your debt. The lower the ratio is, the more capable you are of paying off debt. We have the specifics laid out below, but for more information on what your DTI is and how to calculate it, check out this informational video by our Homeowner Development Manager, Pa Lor:

Take the total of your monthly debt payments and divide that number by your monthly gross income (or monthly net income if self-employed). Then multiply that number by 100 to see the percentage.

(ex: $330 monthly debt/ $2,275 gross monthly income = 0.1450 x 100 = 14.5%)

Keep in mind, your monthly debt does not include things like your rent, insurance payments, or child care expenses.

Monthly Debt ÷ Monthly Gross Income = Debt-to-Income

If this ratio is higher than 18%, you are not currently eligible for Twin Cities Habitat's Homeownership Program. This is because your future home mortgage payment will add to your total monthly debt, and will increase your debt-to-income ratio. If your debt-to-income ratio is below 18%, then you may be considered eligible, but you may still need to focus on debt reduction (paying down loans, credit cards, etc.).

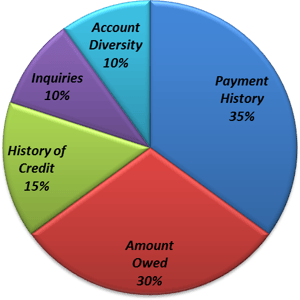

The definition of a credit score is: a number assigned to a person that indicates to lenders their capacity to repay a loan. You receive a credit score from each of the three credit bureaus which are based on some of the following factors:

There are many ways to get your credit score, including through your credit card company and through non-profit counselors. Note that credit scores are not included in credit reports requested through annualcreditreport.com.

It is important to know that the three credit bureaus will report different credit scores. Because of this, Habitat will use the median score reported from the three credit bureaus (Equifax, Experian, and TransUnion). That number must be higher than 580 for each applicant to be considered program eligible. Note: If a client is new to credit or has no credit, that is something their homeownership advisor would be able to help them strategize how to build credit.

If you need help figuring out your income, debt, credit, or other elements you need to apply for our Homeownership Program, visit our Homeownership Resources page today.

Your gift unlocks bright futures! Donate now to create, preserve, and promote affordable homeownership in the Twin Cities.

Credit is one of the most important elements of your financial well-being. It can make all the difference for your life goals, like getting a new...

Before you apply for a mortgage, raising your credit score is one of the best things you can do. That means paying down as much debt as you can. But...

We continue to process the pain and hope of our nation’s uprising for racial justice amid a global health crisis. You can see ourrecent statements...